|

|

|

Article ID: 3402

Last updated: 03 Jun, 2025

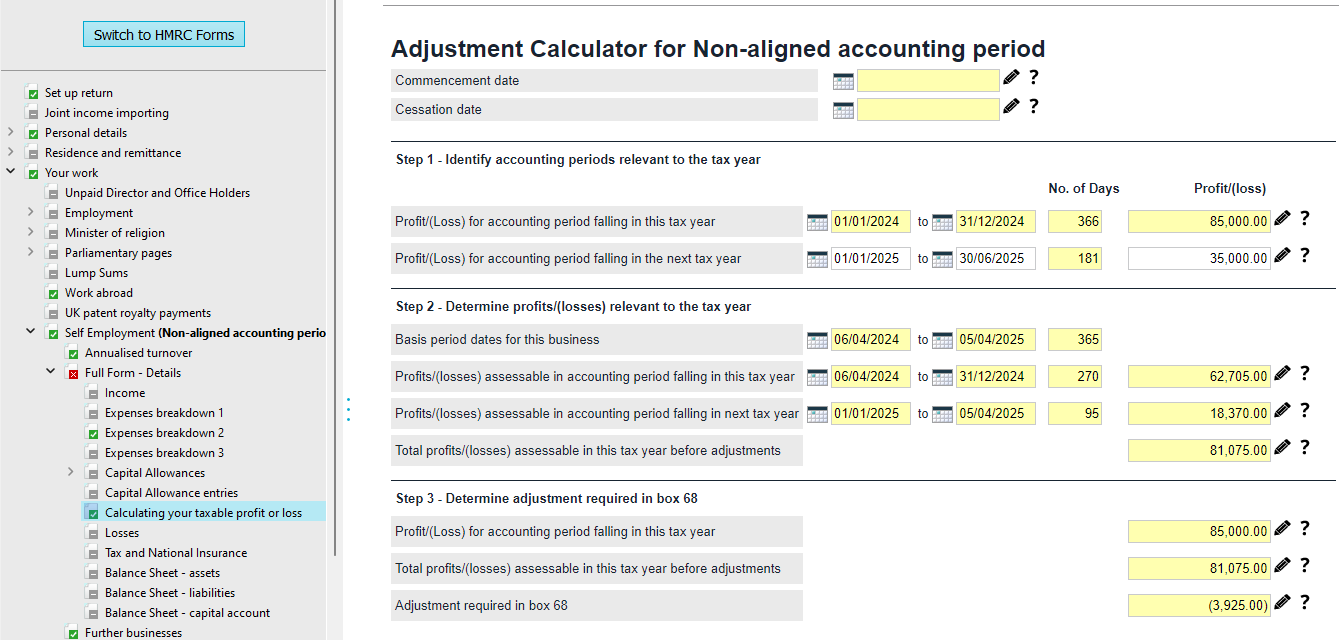

When processing the information for the 2024/25 tax year, the Basis Period Reform will have already taken place. If you are unfamiliar with the rules surrounding this, it is recommended that you review this HMRC webpage for further information. If for any reason, a self employed individual has opted to prepare accounts using a non-aligned accounting period, an adjustment will be required in order to ensure that only profits generated within the tax year are assessed. This will be processed on the self employment full form via the Adjustment Calculator which is available against box FSE68 within TaxCalc (SimpleStep >Your Work > Self Employment > Full Form-Details > Calculating your taxable profit or loss > Adjustment (to arrive at the profit or loss of the taxable period)). Example if you have opted to retain a 31st December accounting period endThe basis period reform would have meant that for the 2023/24 tax year, profits up to 05/04/2024 were recorded and lodged with HMRC. The main accounting period would have been processed as 01/01/2023 - 31/12/2023 with any profits incurred between 01/01/2024 - 05/04/2024 entered as transition profits. When declaring your information for 2024/25, you will enter the main accounting period ending 31/12/2024 on the SA103 self employment tax return pages, with an adjustment to align profits/losses with the tax year. If trading profits for 01/01/2024 - 31/12/2024 are £85,000 and at the point you come to file the tax return, trading profits for 01/01/2025 to 30/06/2025 are £35,000: The adjustment required in box FSE68 would need to:

Once you have entered the accounts figures for the accounting period 01/01/2024 to 31/12/2024, within the Full self employment pages, the adjustment calculator will automatically populate proft/loss for the accounting period. You will then need to enter the additional profits which fall beyond the accounting period. In the example below you will see that profits from 01/01/2025 to 30/06/2025 have been entered.

As you can see, the wizard will apportion the profits (or losses if entered as a negative amount) declared on a daily basis. £85,000 * 270 days / 366 days = profits chargeable between 06/04/2024 - 31/12/2024 of £62,705 £35,000 * 95 days / 181 days = profits chargeable between 01/01/2025 - 05/04/2025 of £18,370 Therefore as profits have been declared on the self employment pages of £85,000 but the total profits assessable for the tax year are £81,075 (£62,705 + £18,370), an adjustment of -£3,925 is required in box FSE68. Should you wish to review more examples, HMRC have some scenarios available on this webpage.

This article was:

|

||||||||||||