|

|

|

Article ID: 3387

Last updated: 25 Mar, 2025

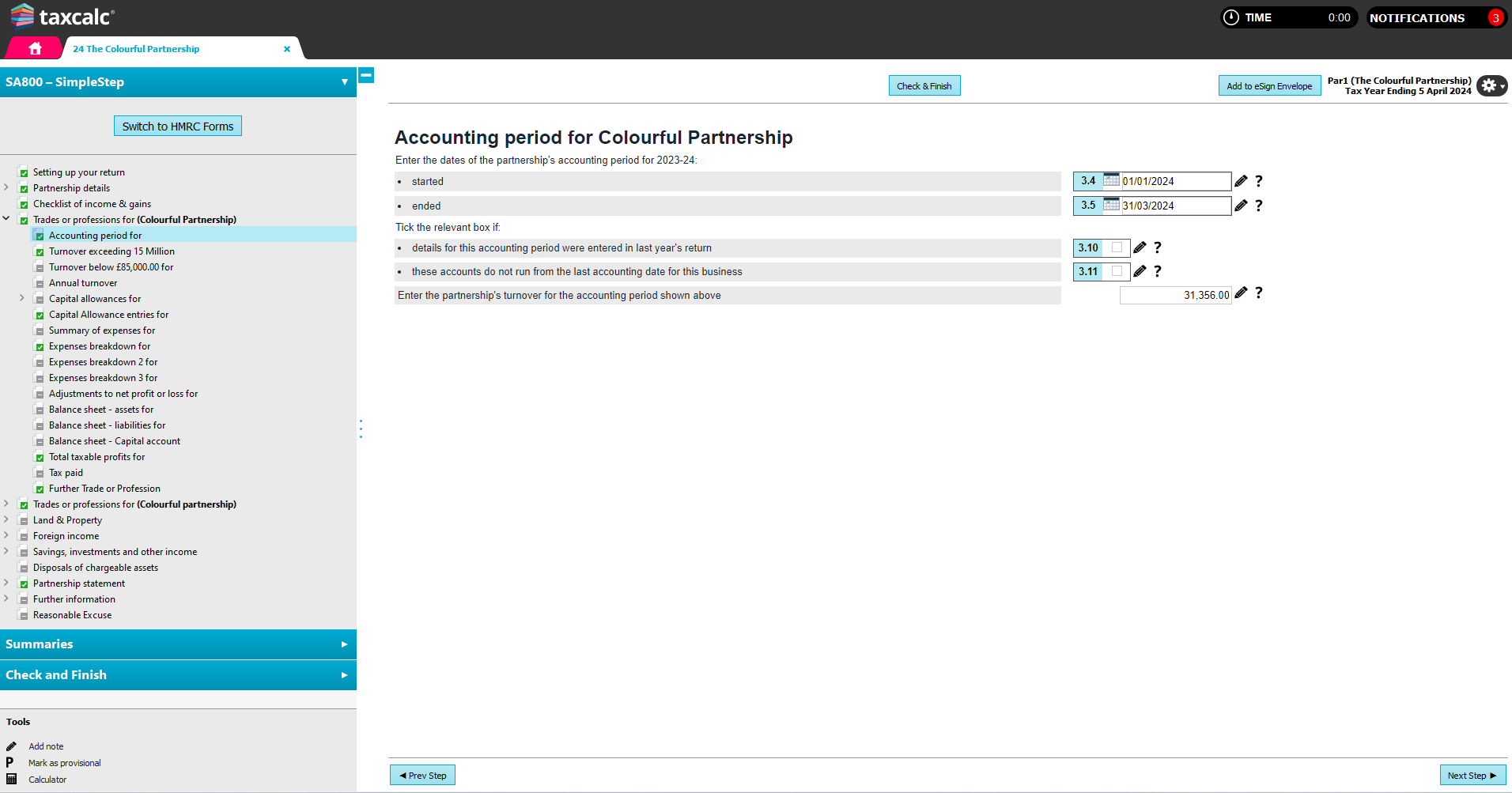

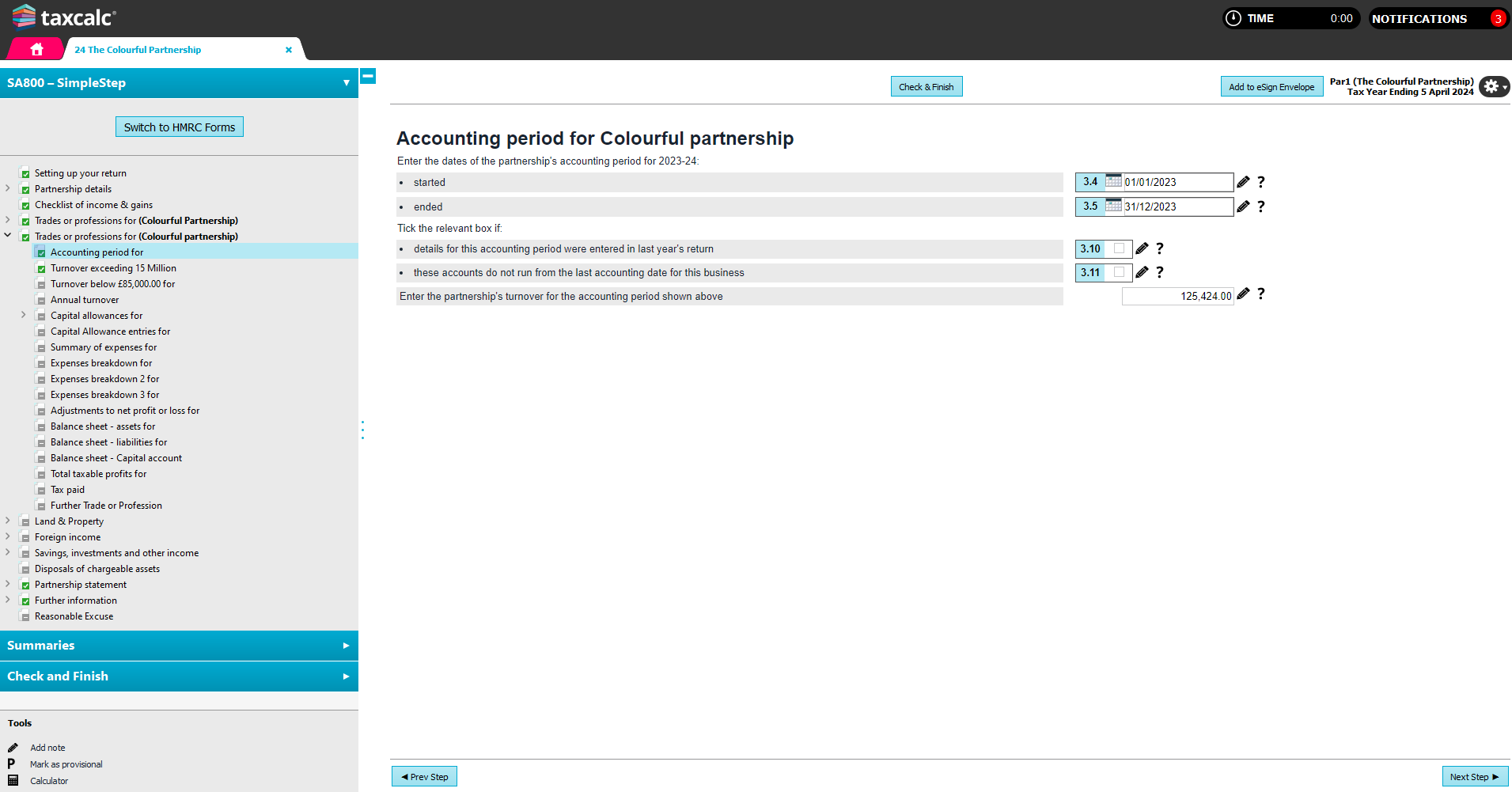

From tax year 2024-25 onwards, individuals that are partners in partnerships will be taxed on their share of profits from the partnership that arise in the tax year that runs from 6 April to the following 5 April (the tax year basis). This replaces the previous current year basis of taxation, which applied up to the 2022-23 tax year, where individuals were taxed based on their share of partnership profits for the partnership accounting period that ended in the tax year. The 2023-24 tax year is a transition year in which any profits or losses from the end of the 2022-23 basis period up to 5 April 2024 will be brought into account. Basis period adjustments, including relief for overlap profits and spreading of transition profits, are calculated separately for each individual partner in the individual partner's tax return. Individual partners may have different basis periods depending on when they joined or left the partnership. How should I complete the SA800 partnership tax return for 2023/24? The SA800 partnership tax return should be completed based on the partnership accounting period or periods that end in the tax year 6 April 2023 to 5 April 2024. In most cases there will be a single accounting period ending in the tax year, however where the partnership has changed accounting date by preparing two sets of accounts there will be two periods and two sets of trading and professional income pages will therefore be required. Example 1 - Partnership accounting period aligns with the tax year. A partnership prepares accounts for the period 1 April 2023 to 31 March 2024, this is the only set of accounts that ends within the 2023/24 tax year and therefore the trading and professional income pages of the partnership tax return should be completed with details of the income and expenses for this period. As the accounting period is aligned with the tax year, the individual partners should not need to make any basis period adjustments in their individual tax returns. Example 2 - Partnership accounting period does not align with the tax year and have decided to not adjust the accounting period to align with the tax year. A partnership prepares accounts to 31 December each year and decides not to change accounting period to align with the tax year. In the 2023/24 tax year there is one accounting period that ends within the tax year, which is the period 1 January 2023 to 31 December 2023. The trading and professional income pages of the partnership tax return should be completed with details of income and expenses for the year ended 31 December 2023. No basis period adjustments are to be made in the partnership return. The partnership statements which the partnership is required to provide to each partner will provide details of the partner’s share of profit or loss for the year to 31 December 2023. The partners will need to make adjustments in their individual tax returns to include their share of profits for the period 1 January 2024 to 5 April 2024. This is explained in more detail in the section below How should an individual that is a partner in a partnership complete their SA100 tax return for 2023/24? Example 3 - Partnership accounting period does not align with the tax year but they decided to adjust the accounting period to align with the tax year. A partnership has historically prepared accounts to 31 December each year. The 2022-23 partnership return was based on the accounts for the year ended 31 December 2022. The partnership decides to change accounting period to align with the tax year in 2023/24 and prepares a single long set of accounts from 1 January 2023 to 31 March 2024. The trading or professional income pages of the partnership tax return should be completed with details of income and expenses for the period 1 January 2023 to 31 March 2024 as this is the only set of accounts that ends in the 2023-24 tax year. The partnership statements will provide details of each partner’s share of profit or loss for the period 1 January 2023 to 31 March 2024. The partners will need to make adjustments in their individual tax returns to adjust for and spread the transition element of profits (relating to the part of the period from 1 January 2024 to 31 March 2024). Example 4 - Partnership A partnership has historically prepared accounts to 31 December each year and decides to change accounting period to align with the tax year in 2023/24. Instead of preparing a single long set of accounts, the partnership prepares two sets of accounts, one for the period 1 January 2023 to 31 December 2023 and one for the period 1 January 2024 to 31 March 2024. In this case there are two accounting periods that end within the 2023/24 tax year and therefore two sets of trading and professional income pages are required. Entering details in TaxCalc SA800 where there are two sets of accounts for the partnership ending in the tax year Continuing Example 4 above, two sets of trading and professional income pages are required;

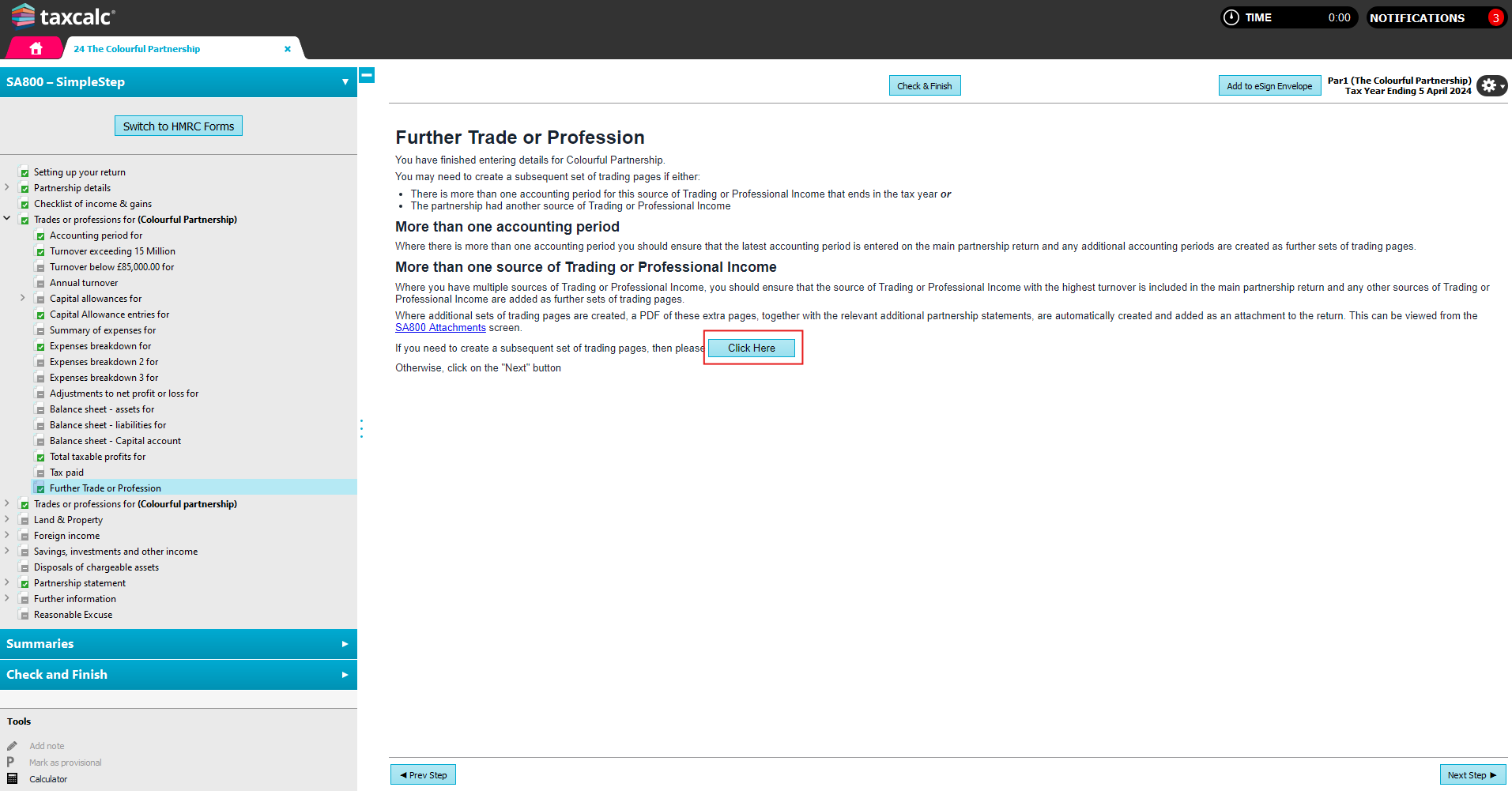

Details for the latest accounting period (in this example the period 1 January 2024 to 31 March 2024) should be entered on the main partnership return, with the earlier accounting period created as a further set of trading pages.

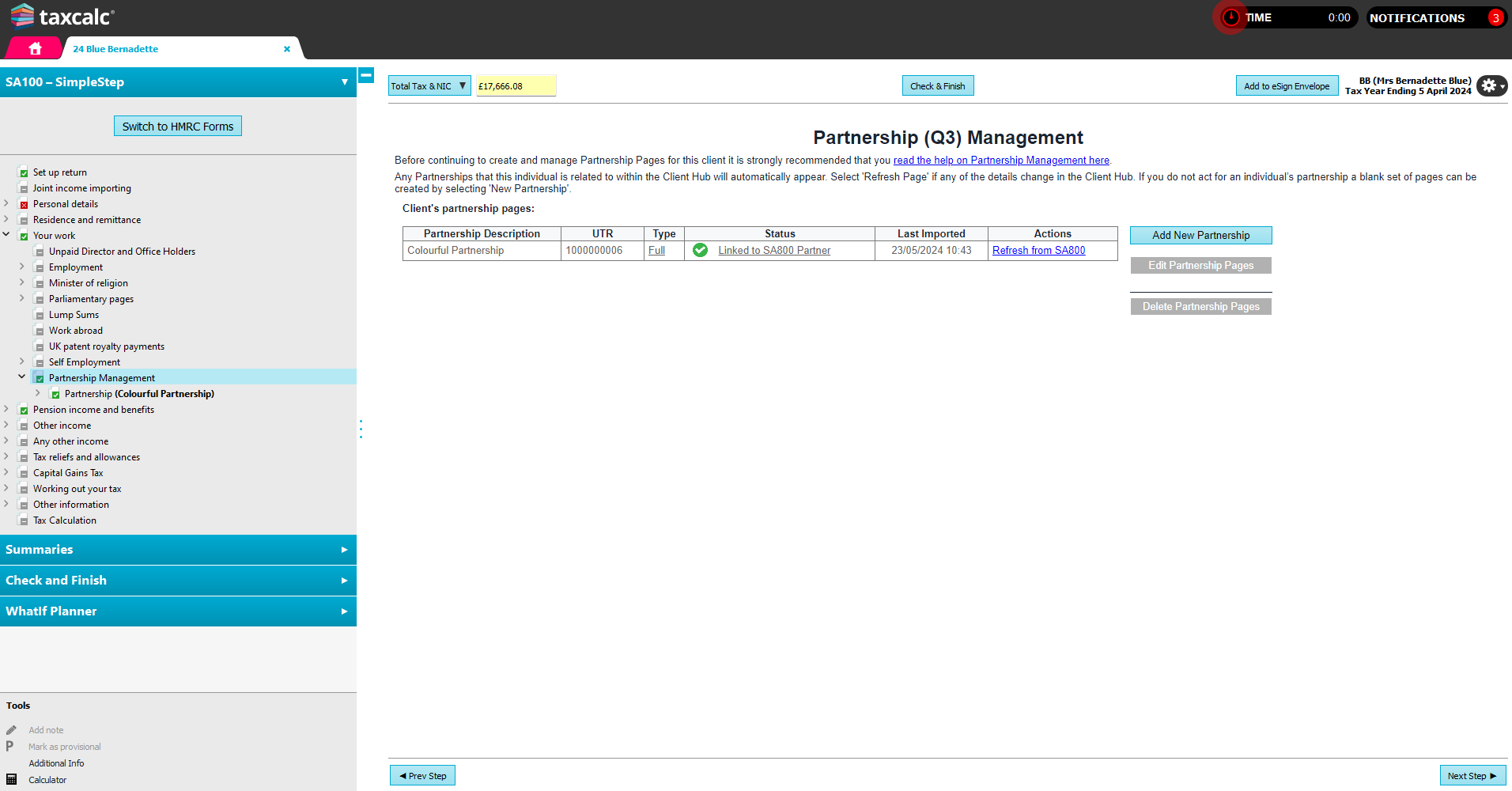

TaxCalc will automatically create the Partnership Trading and Professional Income ‘extra pages’, attached as a PDF attachment to the return. TaxCalc also creates the additional partnership statements for the additional period. These will need to be provided to the partners so that they can prepare their individual tax returns. How should an individual that is a partner in a partnership complete their SA100 tax return for 2023/24? An individual that is a partner in a partnership is required to complete the partnership supplementary pages for their individual self-assessment tax return. There are two versions of the partnership supplementary pages, the Partnership (short) SA104S and the Partnership (full) SA104F. The Partnership (short) pages may be used where the individual does not need to make basis period adjustments or report transition profits and does not need to complete any of the boxes that are only available on the Partnership (full) SA104F pages. Where the partnership did not previously prepare accounts to a date between 31 March and 5 April, it is likely that the individual will need to make adjustments are therefore be required to use the Partnership (full) SA104F pages. In TaxCalc, where the SA800 partnership return has been completed, this will automatically be detected and displayed on the Partnership management screen. The type of pages (full or short) can be changed on this screen as required.

Example 1 A partnership that has prepared accounts for the year 1 April 2023 to 31 March 2024.

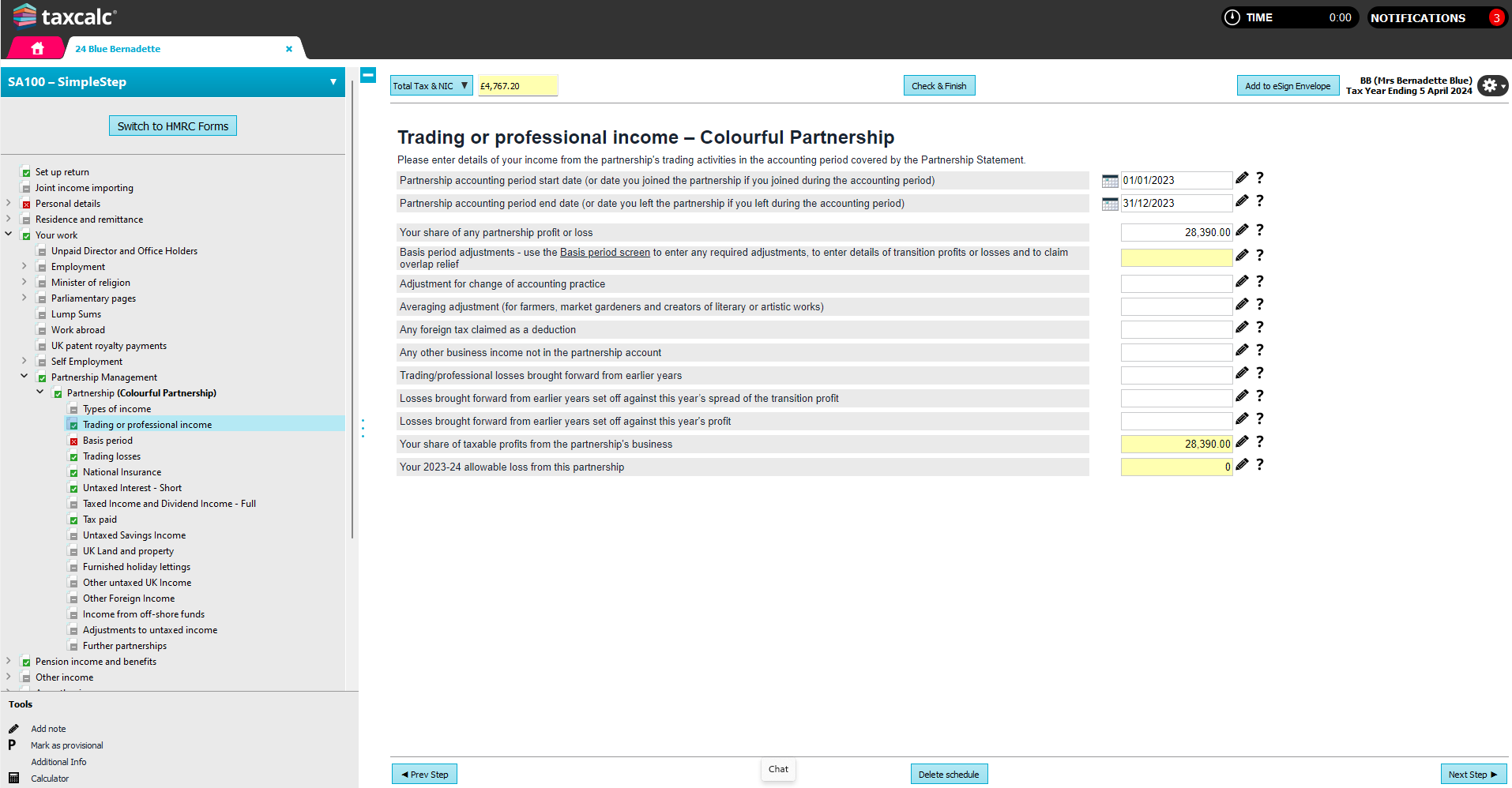

Example 2 A partnership that has prepared accounts for the year ended 31 December 2023 and has not changed accounting date.

In this example, details of the following accounting period (from 1 January 2024 to 31 December 2024) are required so that a proportion (96 days from 1 January to 5 April) of the share of partnership profit can be brought into account. In most cases an estimate will therefore be required of the share of partnership profit or loss for the next period.

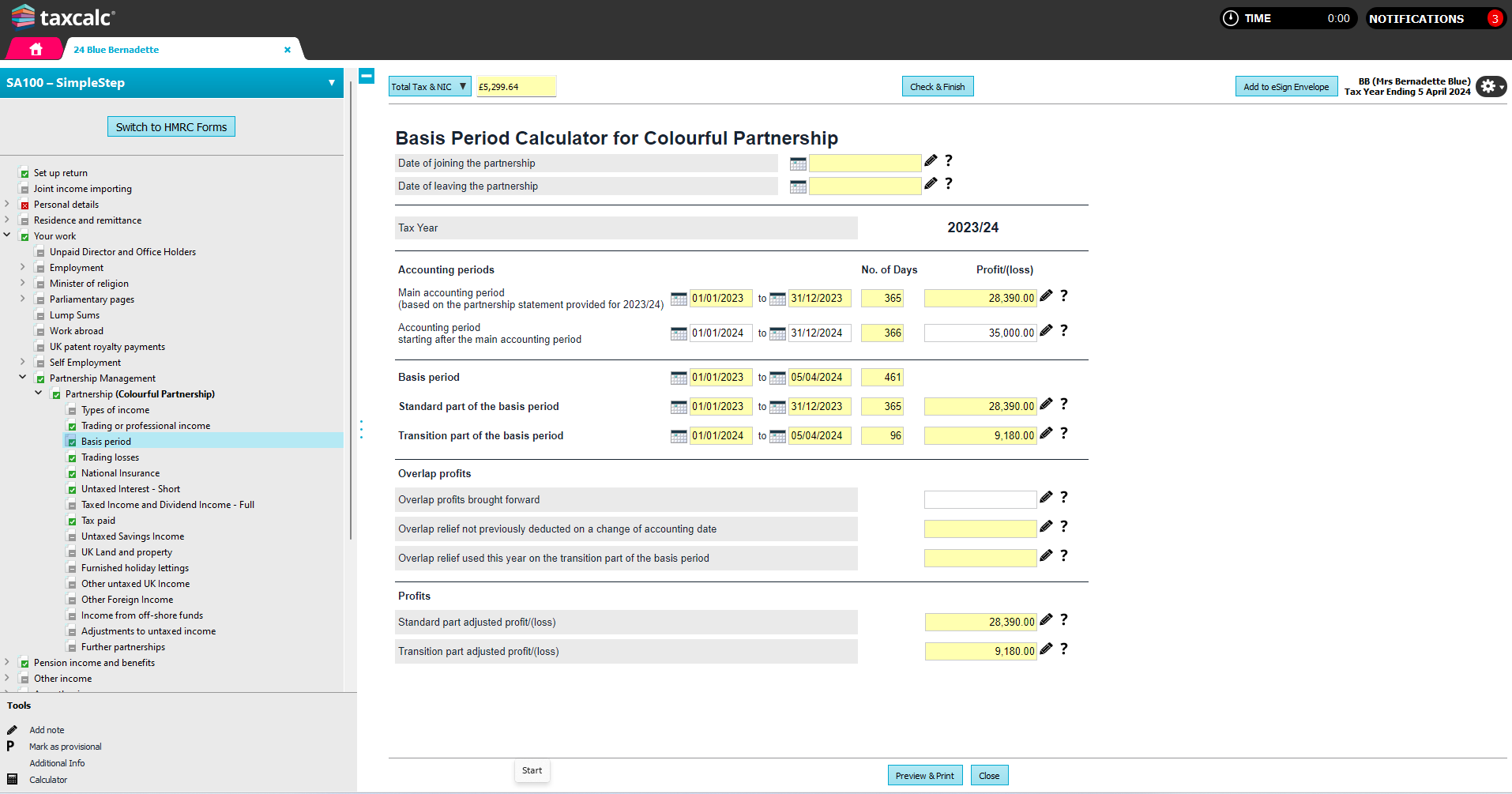

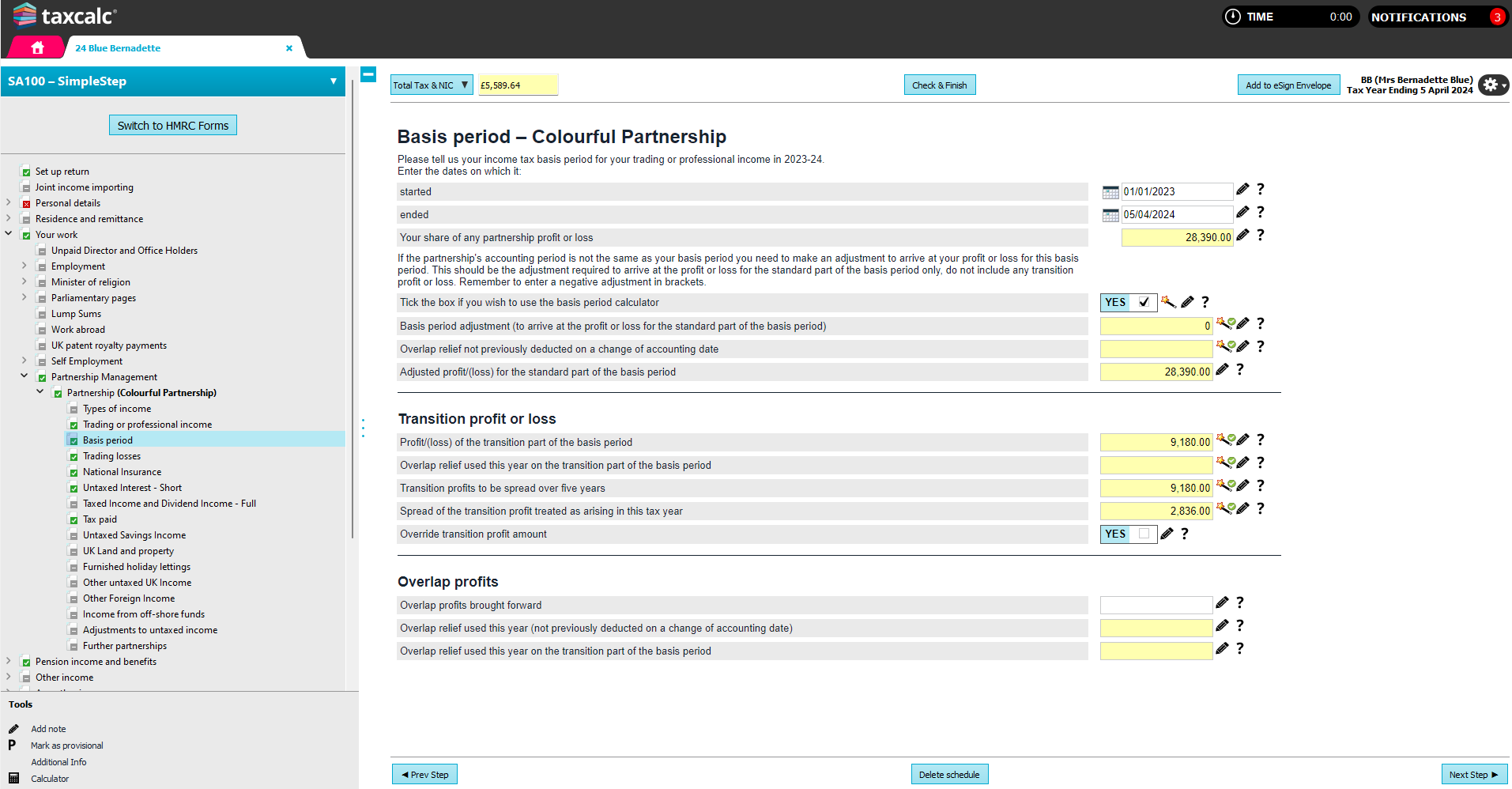

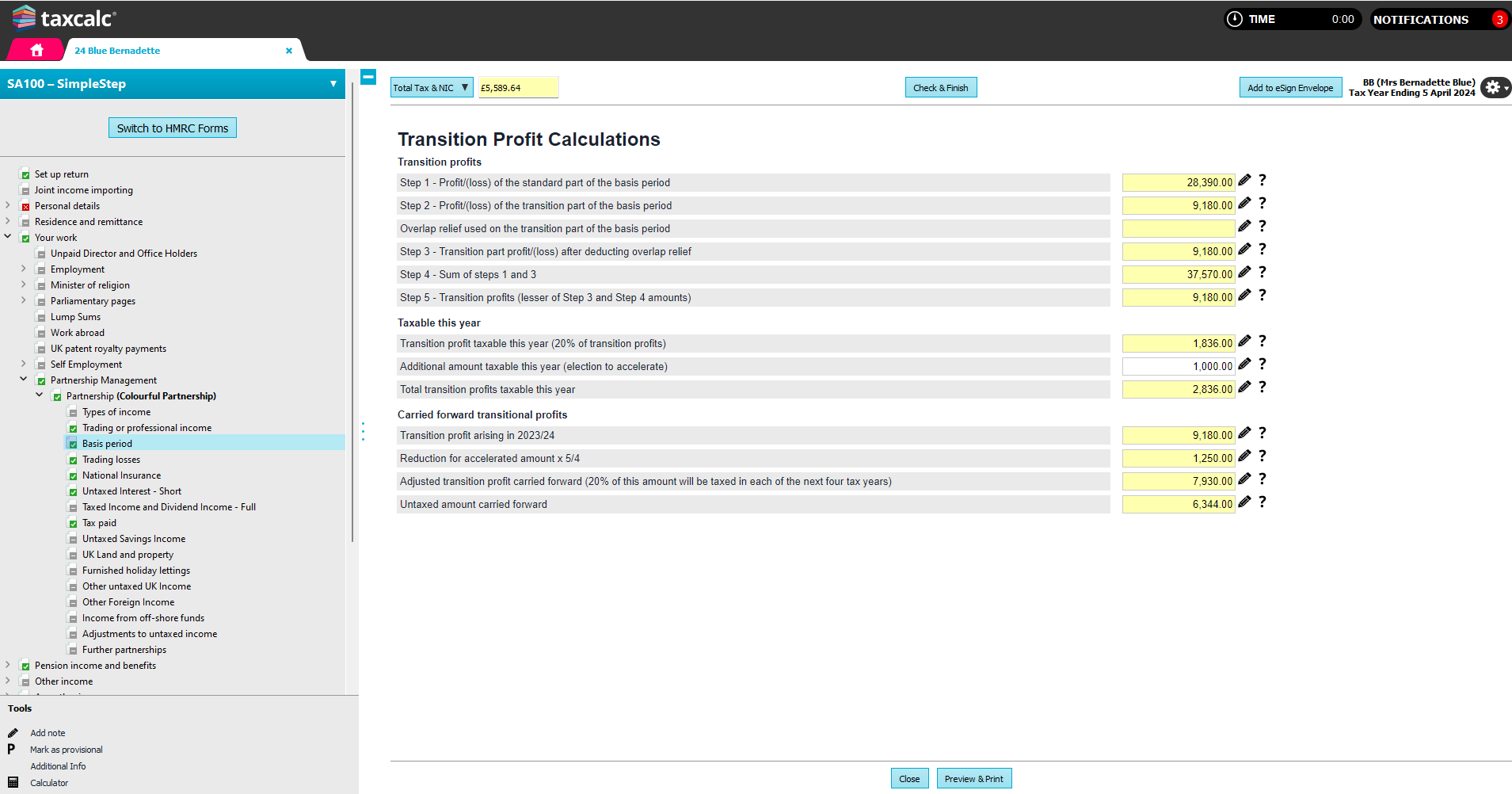

When the basis period calculator has been used, the relevant adjustment and any transition profit or loss will be calculated and displayed on the Basis period screen. The transition profits are spread over five years and the Transition Profit Calculations wizard may be used to enter an Additional amount taxable this year (election to accelerate) where you wish to tax more than the minimum amount of transition profits.

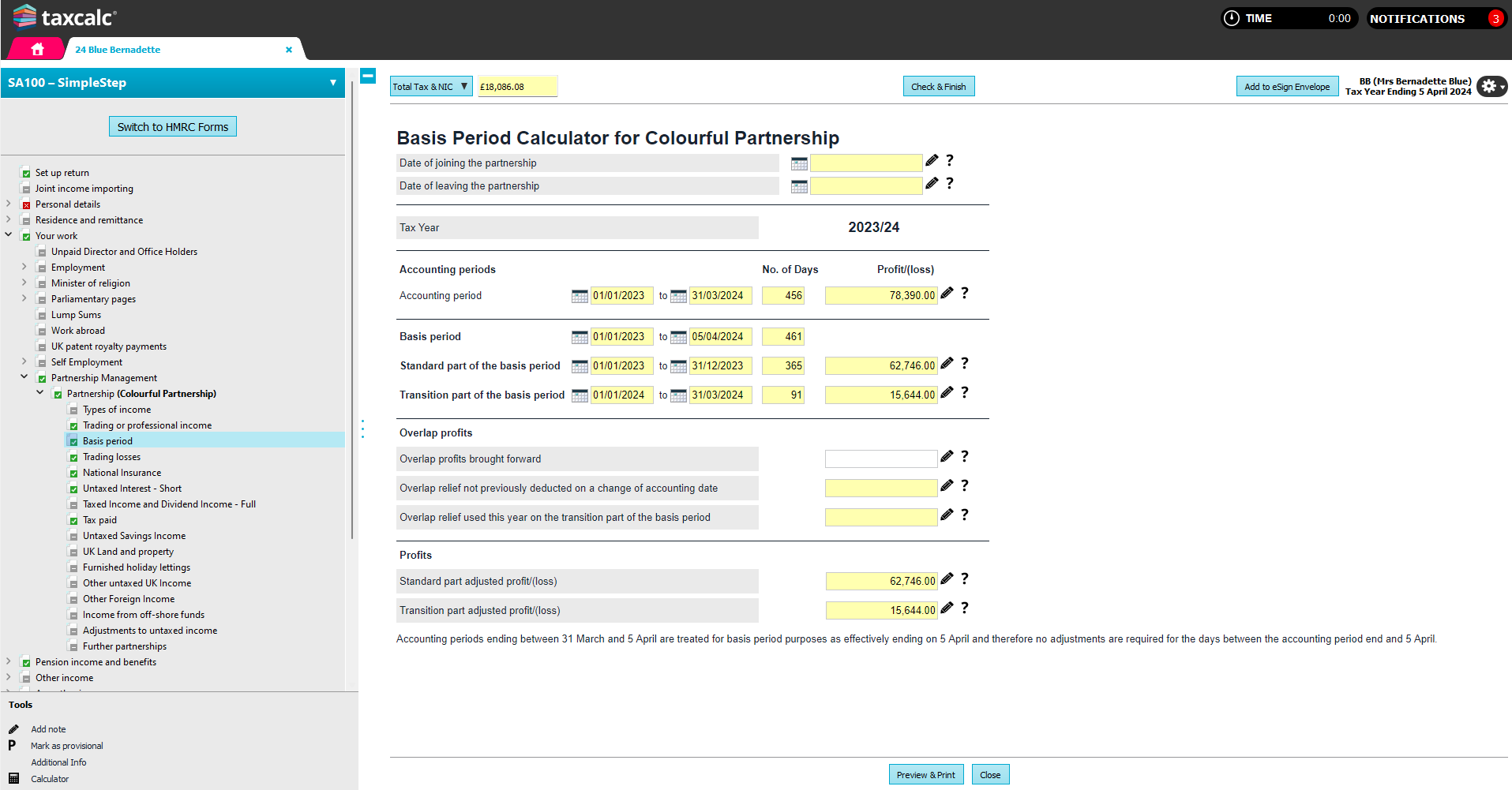

Example 3 A partnership prepares accounts for a long period from 1 January 2023 to 31 March 2024.

Where the basis period calculator is used the transition part of the basis period and the relevant adjustments will be automatically calculated. In this case there are no additional estimated profits to enter as the partnership accounting period covers the whole basis period (days between 1 April and 5 April are effectively ignored).

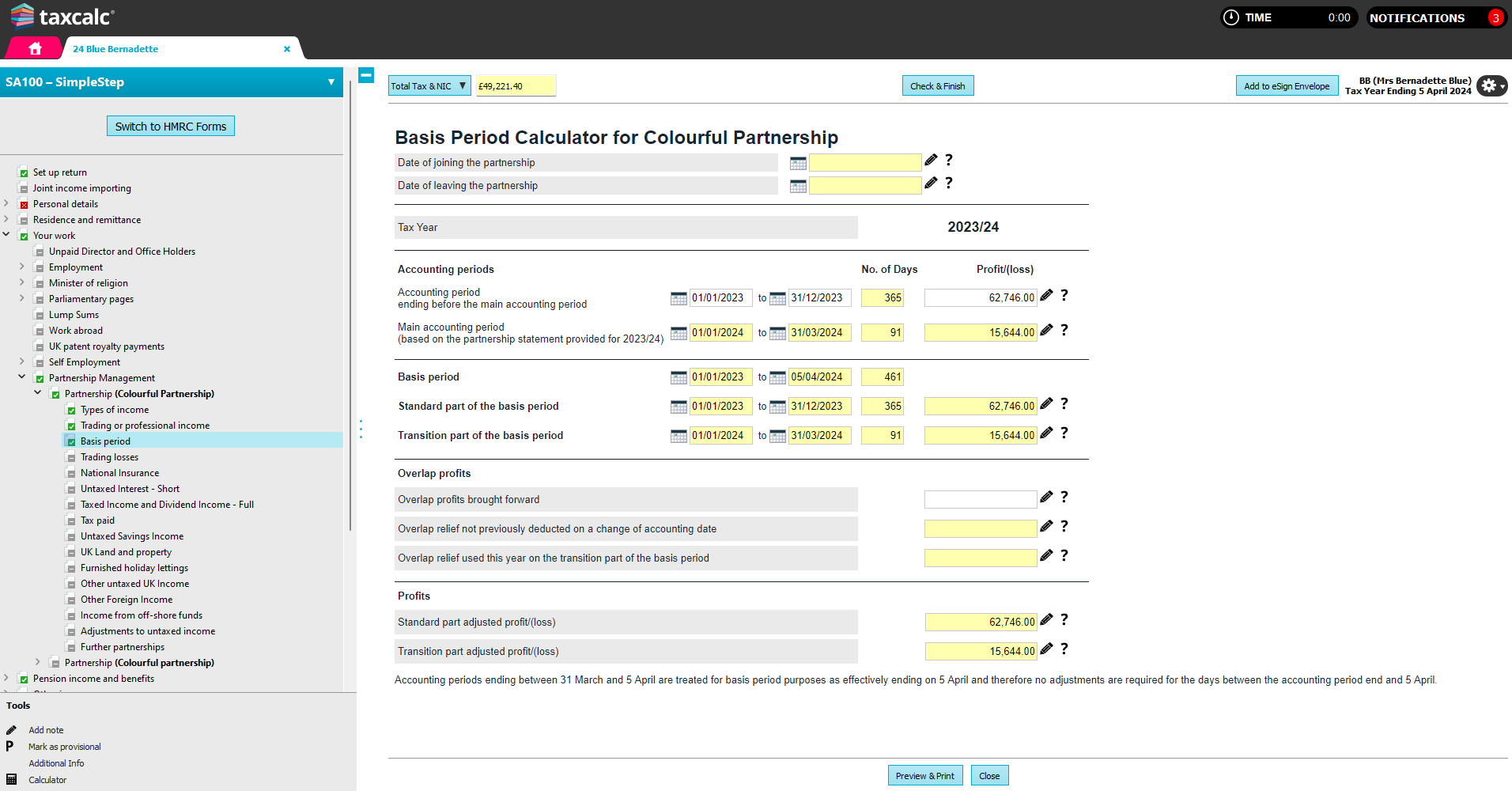

Example 4 A partnership has prepared two sets of accounts; Period 1: 1 January 2023 to 31 December 2023 individual partner’s profit share £62,746 Period 2: 1 January 2024 to 31 March 2024 individual partner’s profit share £15,644 As there are two accounting periods, the partnership will provide two partnership statements to the individual partner, one for each accounting period. The individual partner should prepare one set of partnership supplementary pages SA104(F). The starting point for these should be the latest accounting period, with the relevant adjustments entered to ensure that the correct overall profits are taxed for the tax year.

This article was:

|

||||||||||||