|

|

|

Article ID: 3372

Last updated: 16 May, 2024

TaxCalc April 2024 updatePlease note that the April 2024 update of TaxCalc contains additional functionality for handling multiple accounting periods for the same Self Employment. For details of how to use the additional functionality, see this Knowledge base article. We recommend that you upgrade to the latest version of TaxCalc if you have multiple accounting periods for the same Self Employment as the new version of TaxCalc has automated much of the required work. The steps detailed in this article are relevant where you are running a version of TaxCalc prior to 14.6.300. How should I enter details of multiple accounting periods for a self-employment?From tax year 2024-25 onwards, self-employed individuals will be taxed on the profits that arise in the tax year that runs from 6 April to the following 5 April (the tax year basis). This replaces the previous current year basis of taxation, which applied up to the 2022-23 tax year, where individuals were taxed based on the accounts that ended in the tax year. For individuals that prepare accounts to 5 April each year, or to a date between 31 March and 5 April, the taxable profits will be based on the annual accounts that are prepared in line with the tax year. For example, an individual preparing accounts to 31 March each year will be taxed in the 2024-25 tax year based on the accounts for the year ending 31 March 2025. Where individuals prepare accounts to a date which is not between 31 March and 5 April, it will be necessary to apportion profits or losses from two sets of accounts to calculate the taxable profits for the tax year. The 2023-24 tax year is a transitional year in which any profits or losses from the end of the 2022-23 basis period up to 5 April 2024 will be brought into account. It is possible that two sets of accounts may have been prepared for the 2023-24 tax year when changing accounting date to align with the tax year. HMRC guidance where there is more than one set of accounts for the tax yearHMRC’s published workaround for an individual return with more than one accounting period is as follows; “Where there is more than one set of accounts for 2023-24, separate Self Employment pages should be completed for each set of accounts. One set of Self Employment pages should be completed with details of the latest accounting period and FSE66 to FSE82 as appropriate, should be completed to arrive at the taxable profit for the basis period. Additional Self Employment pages for any other accounting periods should be submitted as an attachment with an explanation given in white space (additional information). Note: that where the pages do not include the full details of profits, expenses necessary to confirm the net profit the return does not satisfy the requirements of Section 8 TMA1970.” For tax returns that are to be filed online;

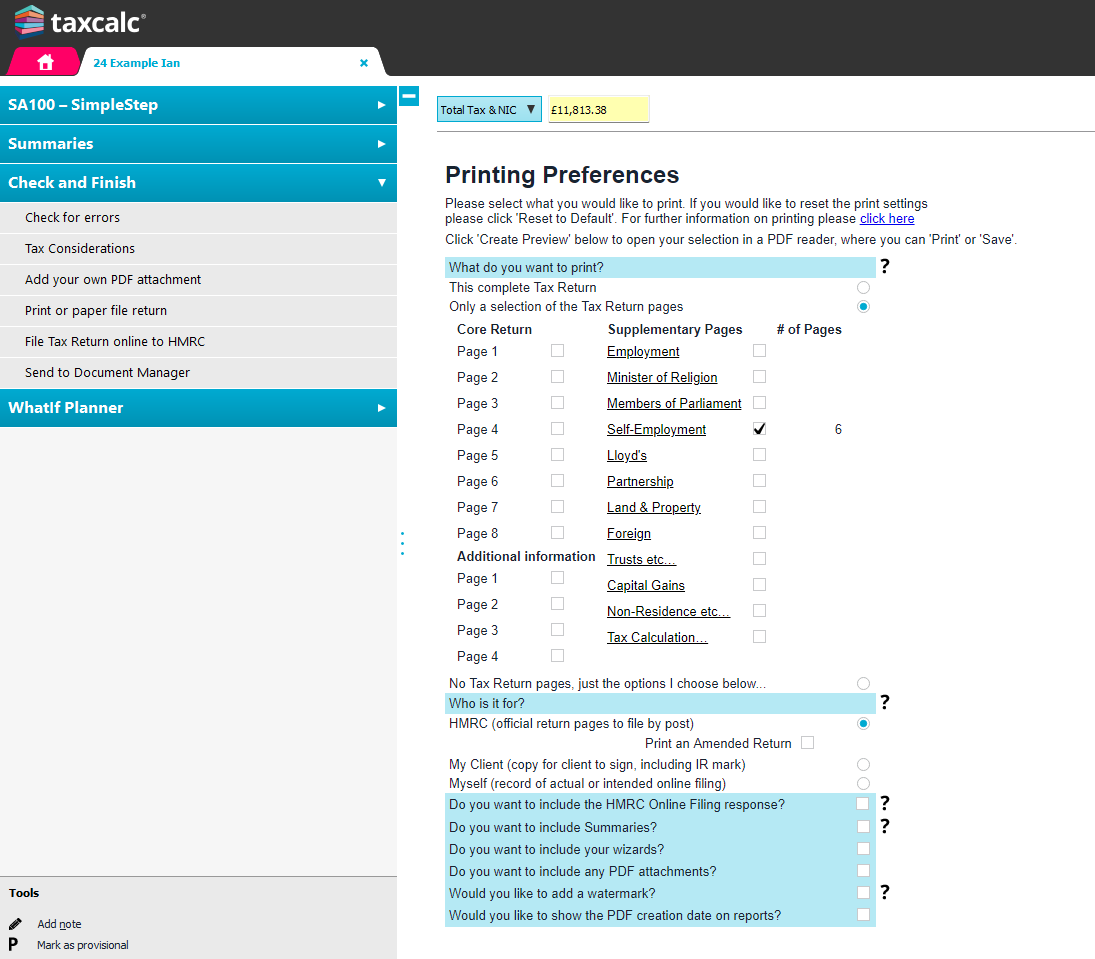

How do I complete the entries using TaxCalc?We recommend using HMRC Forms mode to check the specific box entries for the adjustments, so we have produced the following guidance referring to HMRC Forms mode, rather than SimpleStep entries. The following example is used to demonstrate the process using TaxCalc. A self-employed trader prepares accounts to 31 December each year. The basis period for the 2023-24 tax year runs from 1 January 2023 to 5 April 2024. One set of accounts is prepared for the year to 31 December 2023 and a separate set of accounts is prepared for the three months from 1 January 2024 to 31 March 2024. Step 1 – Prepare self-employment pages for the first accounting period For our example, this is the accounting period 1 January 2023 to 31 December 2023. Create self-employment pages. Enter details of income, expenditure and capital allowances for the first accounting period up to page 3 . Ensure that details entered only relate to the first accounting period, in our example this is the year to 31 December 2023. Do not enter any basis period or other adjustments on page 4. Complete the Balance Sheet information on page 5 if required. Partnerships: in the SA800 create two trade pages, one for the standard part of the basis period and one for the transitional part. In this example the transitional accounting period will be from 01/01/2024 to 31/03/2024. Import from the SA800 into the SA100. Two SA104 (partnership pages will be created. Step 2 – Create a PDF copy of the self-employment pages for the first accounting period Once you are satisfied that all details for the first accounting period have been entered correctly, create a PDF copy of the self-employment pages. You can do this from the Check and Finish section in TaxCalc. The Printing Preferences screen includes an option to only print a select of the Tax Return pages. Within this option you can choose to only print the Self-Employment pages, from which you can then create a PDF.

Partnerships: Create a PDF of the SA104 page containing data for the standard part of the period, in this example will be 1 January 2023 to 31 December 2023. Step 3 – Create the self-employment pages for the second accounting period Another set of full self-employment pages should be created for the second accounting period. Ensure that you enter the accounting period start and end dates correctly on page 1 (in our example this is 1 January 2024 to 31 March 2024). Income, expenditure and capital allowances entered should be for the second accounting period only. If you have any capital allowance pool values carried forward from the first accounting period, these will need to be entered as brought forward balances in the second accounting period. Partnerships: this will already be created after importing from the SA800. Step 4 – Enter the correct basis period adjustments Ensure that the correct basis period start and end dates are entered on page 4 of the second set of self-employment pages. For our example these are 01/01/2023 and 05/04/2024. The adjustment entered in box 68 should be an amount which, when added to the net business profit or loss per the second accounting period, gives the correct overall profit or loss for the standard part of the basis period. The amount entered in box 73.1 should be the calculated profit or loss of the transition part of the basis period. The Basis period calculator wizard can be used to assist with calculating the required adjustment in box 68 and transition profit or loss to be included in box 73.1. To use the Basis period calculator wizard, select the option ‘Tick the box if you wish to use the basis period/overlap calculator’, either from the Basis Period screen in Simple Step or from Page 4 of the Self-employment pages in HMRC Forms mode. Within the Basis period calculator wizard, details for the second accounting period will automatically be displayed. Enter details for the first accounting period (based on the PDF created at step 2) using the ‘Accounting period ending before the main accounting period’ entries. In our example this is the period 01/01/2023 to 31/12/2023. The profit or loss to enter should either be the profit per box 64 from the first accounting period or the loss from box 65. Enter a profit as a positive figure and a loss as a negative. The Basis period calculator will automatically calculate the standard and transition part profit or loss and any necessary adjustment for inclusion in box 68.

Partnerships: The above instructions remain the same in principle for the SA104, apart from the box numbers. Enter the adjustment to the standard part of the period in box 9 and enter the same amount (transitional profits) into box 16.1. Step 5 – Complete the additional information box Use the ‘Any other information’ box on Page 6 of the supplementary pages to explain that the workaround for two accounting periods covering the tax year has been used. Step 6 – Attach the PDF from step 2 to the return prior to submission Before submitting the tax return, ensure that you attach the PDF that was created at Step 2. This can be added in the Check and Finish section of TaxCalc. Click on Attach, Add PDF and follow the on-screen instructions. Step 7 – Delete the self-employment pages for the first accounting period Before submitting the tax return, ensure that you delete the self-employment pages for the first accounting period from the return. For our example this is the period 01/01/2023 to 31/12/2023. Partnerships: Delete the SA104 for the standard part of the period. For our example this is the period 01/01/2023 to 31/12/2023.

This article was:

|

.png)