|

|

|

Article ID: 3087

Last updated: 06 Sep, 2023

What is Top Slicing Relief?Top Slicing Relief (TSR) hypothetically spreads a chargeable event gain (CEG), such as a gain on a life policy, over the years of the policy, such that the tax is payable as if the CEG had been received in equal amounts every year. It’s not an exact calculation as it doesn’t match the income to the actual tax years, but it gives a good approximation. How is TSR calculated?The law (ITTOIA 2005 s 535 to 537) requires the taxpayer to perform two calculations:

TSR is the difference between the two resulting figures. What has changed for CEGs arising in 2019/20 since the Finance Bill 2020 update?Following a successful challenge by a taxpayer (the Silver case). the Finance Bill 2020 includes amendments to sections 535 to 537 which confirms that for the purpose of calculation 2:

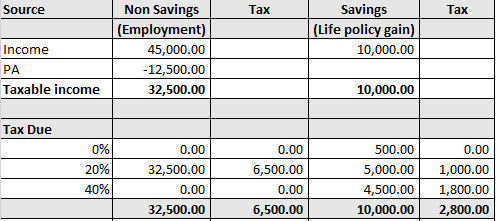

How is Taxcalc calculating TSR for 2019/20 returns?HMRC is not changing their online filing system's TSR calculation for the Finance Bill 2020 update and consequently we are following HMRC's methodology for TSR calculations for the 2019/20 tax year to ensure that our customers can continue to file online.This means that applicable gains arising during the 2019/20 tax year will potentially require a revised calculation to ensure the correct tax is paid. How is Taxcalc calculating TSR for 2020/21 , 2021/22 and 2022/23 returns?Whilst HMRC changed their online filing system's TSR calculation for these periods for the reinstatement of the personal allowance, the system was not updated for the recalculation of the personal savings allowance or the starting rate for savings. To allow our customers to continue to file online, we are following HMRC methodology. This means that gains arising during these periods may require a revised calculation, if the personal savings allowance and starting rate for savings allowance would be increased for the annualised gain calculation. How does this effect filing the return?2019/20 returns : HMRC will be treating these scenarios as Exclusions (reference 116) for filing purposes, giving an option to file a paper return as this is a reasonable excuse for not filing online. TaxCalc provides a Check and Finish message for those scenarios which will explain how to proceed with filing the return. 2020/21 , 2021/22 and 2022/23 returns: HMRC will be treating these scenarios as Exclusions (reference 140) for filing purposes, giving an option to file a paper return as this is a reasonable excuse for not filing online. Whether the return is filed online or by post, we advise that the Exclusion number 116 or 140 is referenced either on the return or with a covering letter. This will alert HMRC to identifying that a revised calculation summary will need to be issued. On the return, Exclusion information can be entered into either Forms mode or SimpleStep via: Tax Calculation>Page 2>Any other information (box 17). In addition, if there is supporting documentation to be added, including a revised manual calculation, this can be added as a pdf in Check and finish> Add your own PDF attachment, and click on 'Add PDF'. How will the changes affect previous years' calculations of TSR?Since the initial announcement HMRC have agreed concessionary treatment for the calculation changes to apply to all CEGs arising in 2019/20. Furthermore, within their Agent Update -issue 79, they have stated that the changes will also apply to gains reported in 2018/19 returns. This is an extension of the position in Agent Update 78, which indicated that HMRC would only be applying the new Finance Bill provisions to 2019/20 gains. Example of how TSR is calculated for gains since the Finance Bill 2020 changesIn 2019/20 Tom has taxable employment income of £45,000. He has a chargeable event gain of £70,000 on the full surrender of a life insurance policy which he has held for 7 years. As this is a UK policy, basic rate tax will be treated as having been paid on the amount of the gain, in this case £14,000 (£70,000 @ 20%). For 2019/20, higher-rate tax applies when taxable income exceeds £37,500. As Tom is a higher rate taxpayer this year, his personal savings allowance is £500. Tom's total income is £115,000 so his personal allowance is reduced by £7,500 to £5,000. The starting rate for savings will not be due as Tom’s total non-savings income above the personal allowance exceeds £5,000. Step 1: Calculate the total taxable income for the year and identify how much of the gain falls within the starting rate for savings, personal savings allowance nil rate, basic, higher or additional rate bands as appropriate.

Step 2: Calculate the total tax due on the gain across all tax bands. Deduct basic rate tax treated as paid to find the individual’s liability for the tax year. Total tax chargeable on the gain £27,800 Less Basic Rate tax treated as paid (£14,000) Total liability for the year £13,800 Step 3: Calculate the annual equivalent of the gain. The annual equivalent is calculated by dividing the gain by the number of years the policy has been held (N). In this case the annual equivalent is £70,000 / 7 = £10,000. Step 4: Calculate the individual’s liability to tax on the annual equivalent. Since 11 March 2020, the amount of the personal allowance used in the top slicing relief calculation is set by virtue of the taxpayer’s adjusted net income for the tax year, using the 'sliced gain'. Prior to this the personal allowance used in the top slicing relief calculation was set by virtue of the taxpayer's adjusted net income for the tax year, based on the total gain. The savings starting rate and personal savings allowance used in the top slicing relief calculation continue to be set by virtue of the taxpayer’s adjusted net income for the tax year, using the total gain. Then, deduct basic rate tax treated as paid on the annual equivalent and multiply the result by N. This gives the individual’s relieved liability.

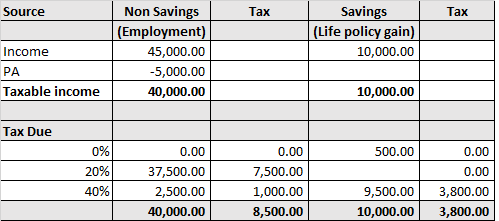

Less Basic Rate tax treated as paid on slice (£2,000) Total liability for one year £ 800 Multiply by N (7) £5,600 Step 5: Deduct the individual’s relieved liability at step 4 from the individual’s liability at step 2 to give the amount of top slicing relief due. TSR is the difference between the total liability and relieved liability: Total liability £13,800 Annualised liability £ 5,600 Top Slicing Relief £ 8,200 How would TSR be calculated before the Finance Bill 2020 changes?Step 4:Using the same example as above, the key difference is that the personal allowance would be restricted to the tapered allowance of £5,000 used for the main calculation:

Total tax chargeable on the sliced gain £3,800 Less Basic Rate tax treated as paid on slice (£2,000) Total liability for one year £1,800 Multiply by N (7) £12,600 Step 5: Total liability £13,800 Annualised liability £12,600 Top Slicing Relief £ 1,200

This article was:

|

.JPG)