|

|

|

Article ID: 2867

Last updated: 06 Mar, 2024

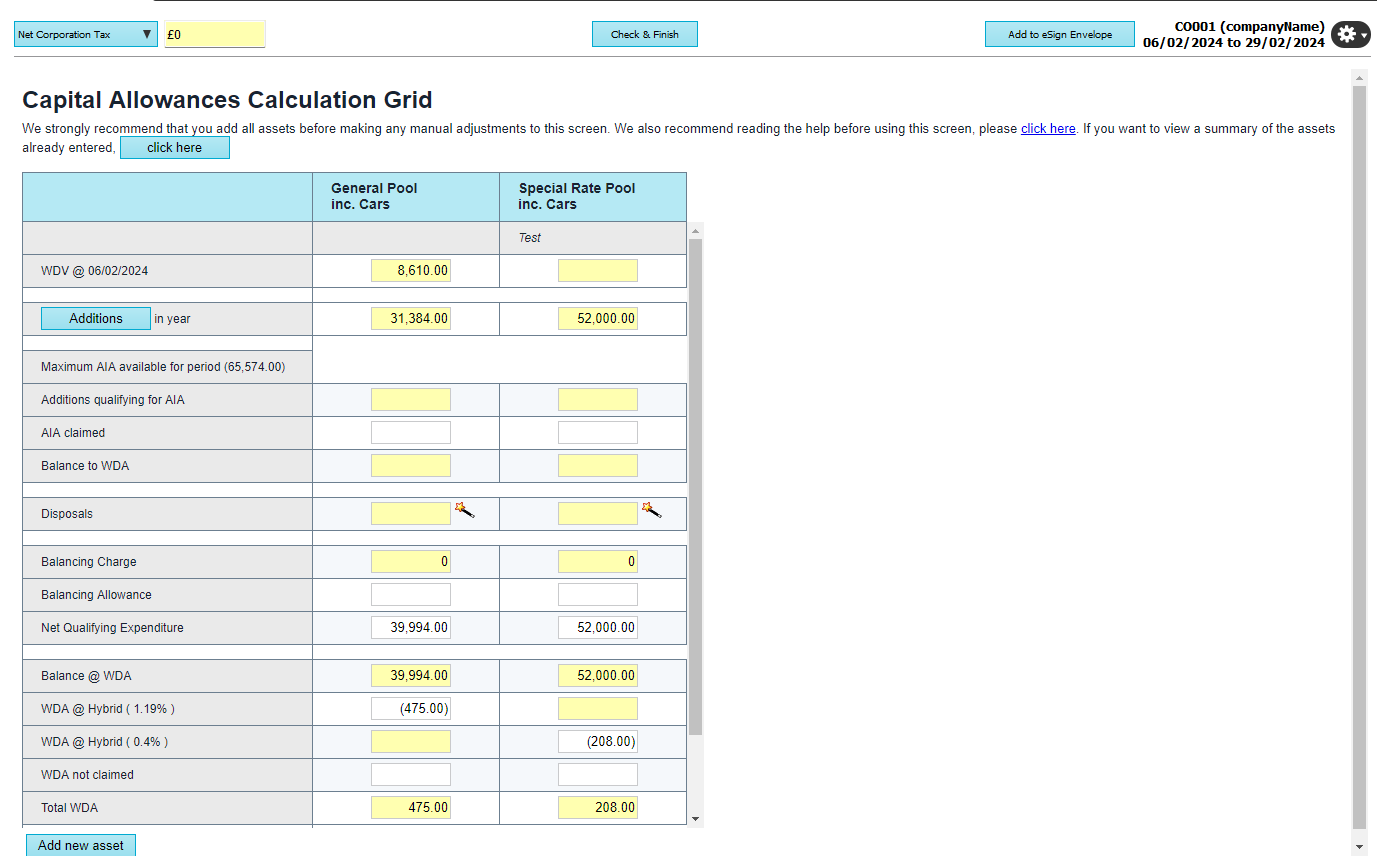

HMRC will issue the rates available for each pool based on the full tax year. If you have a scenario where a tax return is covering a period other than a tax year, you will see the term Hybrid present on the Capital Allowance Calculation Grid. This is because the application will complete the pro rata calculation based on the number of days present (which will therefore account for leap years too). A scenario to explain this further has been detailed below for your convenience. A limited company was formed on 06/02/2023 and are preparing accounts to 29/02/2024. The first limited company tax return will cover the period 06/02/2023 - 05/02/2024 and the second will cover the period 06/02/2024 - 29/02/2024. For the period 06/02/2023 - 05/02/2024, the full rates for the pools would be available as a full tax year is being covered. For the second period, the rates available would need to be pro-rated as the return only covers 24 days. If we take the General pool where the full rate available is 18%, we would take the 18% and divide this by 366 days (as this is a leap year) and multiply this by the 24 days applicable to provide the rate (rounded up to the nearest decimal place as per HMRC rules) of 1.19% Similarly for the Special Rate pool where the full rate available is 6%, we would take the 6% and divide this by 366 days (as this is a leap year) and multiply this by the 24 days applicable to provide the rate (rounded up to the nearest decimal place as per HMRC rules) of 0.4%

This article was:

|