Inputting trading and property income on a CT600

Follow these steps to input trading and property income on a CT600 form:

SimpleStep: CT600 Core > Trade and professional income > Tax adjusted profit/loss-disallowable expenditure

HMRC Forms: CT600 Core > Computations > Tax adjusted profit/loss-disallowable expenditure

Both SimpleStep and HMRC Forms follow the same six steps that are outlined below:

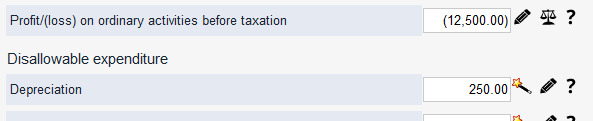

- Enter the figure for Profit/(loss) on ordinary activities before taxation – this is the total of trading profit/(loss) and property profit/(loss).

- Enter Disallowable expenditure (Depreciation).

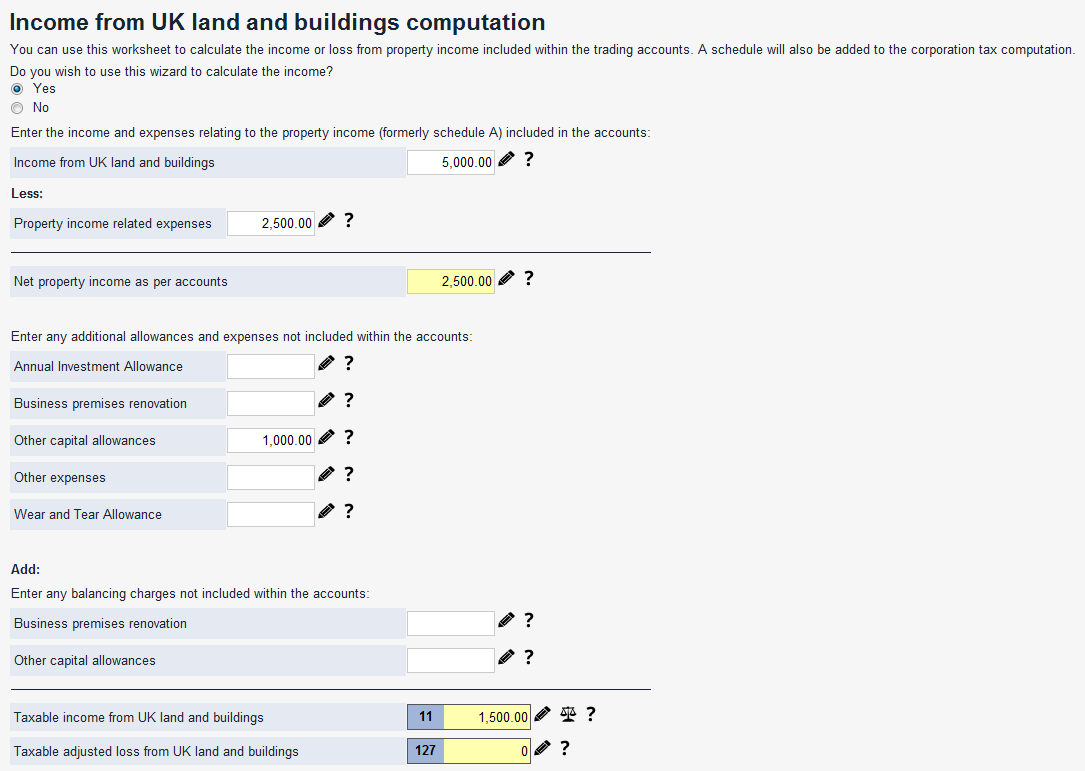

- Go to Tax adjusted profit/(loss) worksheet – other adjustments > Income from UK land and buildings.

- Enter Income from UK land and buildings – this is the rent received, before expenses.

- Enter Property income related expenses – this is the total expenses included in the profit/(loss) figure in Step 1.

- Enter Other capital allowances – this is any additional expenses not included in calculating the profit/(loss) figure.

Worked example

This example shows you how to complete a CT600 form using the following trading and property income figures:

- Trading loss = £15,000

- Disallowable expenditure (depreciation) = £250

- Taxable trading loss = £15,000 - £250 = £14,750

- Rent received = £5,000

- Rental expenses = £2,500

- Capital allowances/other expenses = £1,000

- Taxable property income = £2,500 - £1,000 = £1,500

Calculate and enter the following figures (see diagram):

- Profit/(loss) on ordinary activities before taxation = £(15,000) + £5,000 - £2,500 = £(12,500)

- Disallowable expenditure (Depreciation) = £250

Go to Tax adjusted profit/(loss) worksheet – other adjustments > Income from UK land and buildings and enter the following figures (see diagram):

- Income from UK land and buildings = £5,000

- Property income related expenses = £2,500

- Other capital allowances = £1,000

Note: If you enter Income from UK land and buildings net of expenses (that is, as £5,000 - £2,500 = £2,500), then you don’t need to enter Property income related expenses.